Causes of inflation: what drives prices higher

Prices have a way of rising faster than wages, savings, and expectations. What is less obvious is the reason – and why the same economy can experience inflation for completely different reasons at different points in time.

On this page

In any functioning economy, prices are always moving. Inflation occurs when prices rise persistently and broadly enough to reduce what money can buy. Central banks, governments, and businesses track it closely because sustained inflation reshapes behavior: it changes how people spend, save, invest, and negotiate wages.

What is inflation and why it matters

What causes inflation, at the most basic level, is an imbalance between money and goods. When the amount of money circulating in an economy grows faster than the supply of things to spend it on, prices adjust upward. That adjustment is inflation.

Debtors benefit when inflation erodes the real value of what they owe; savers lose ground if returns don't keep pace. Workers on fixed wages fall behind; those with pricing power or indexed contracts fare better. Real estate and equity owners often see nominal values rise. Cash holders don't.

For that reason, inflation is treated as a core economic indicator rather than just a price statistic. Most central banks target around 2% – low enough to avoid distorting decisions, high enough to give monetary policy room to maneuver. Too high, and it disrupts planning and erodes living standards. Too low or negative, and it can signal stagnation or tip into deflation, which carries its own risks.

Main forces that drive inflation

Inflation causes are usually grouped into a few broad categories, though in practice they overlap and reinforce each other.

Demand-pull inflation occurs when consumer or government spending outpaces the economy's ability to supply goods and services. Strong employment, rising incomes, or fiscal stimulus can all generate this kind of pressure. The post-pandemic recovery of 2021 to 2022 is a recent example: stimulus payments, pent-up demand, and a rapid reopening collided with constrained supply, pushing prices sharply higher across multiple categories simultaneously.

Cost-push inflation works from the supply side. Higher energy prices or supply chain failures raise production costs, and those costs move into retail prices. The oil shocks of the 1970s are the classic example; more recently, the disruption to global semiconductor and shipping networks during the pandemic produced similar dynamics in specific industries.

Wage-driven inflation sits at the intersection of both. Higher wages increase household spending power, which drives demand; they also raise the cost of production, which pushes prices up from the supply side. In tight labor markets, this can become self-reinforcing: workers demand higher wages to keep up with rising prices, which feeds further price increases. Economists call this a wage-price spiral, and central banks watch for it closely because it is difficult to unwind without deliberately cooling the labor market.

Monetary conditions also play a major role. When money supply grows faster than the economy's productive capacity, prices absorb the difference. Milton Friedman's observation that inflation is always and everywhere a monetary phenomenon captures this logic, though most economists now treat monetary policy as one input among several rather than the sole determinant.

Inflation expectations are less visible than oil shocks or wage growth, but they can be just as important. When households and businesses expect prices to rise, they act accordingly: workers negotiate higher wages, companies raise prices preemptively, and contracts build in escalators. Those actions then produce the inflation that was anticipated. Expectations are self-fulfilling in a way that makes them difficult to dislodge once they become entrenched – which is why central bank communication around targets and credibility matters as much as the actual policy rate.

Because these forces overlap, economists rely on several measures to understand where inflation is coming from and how broad it has become.

How inflation is measured in the economy

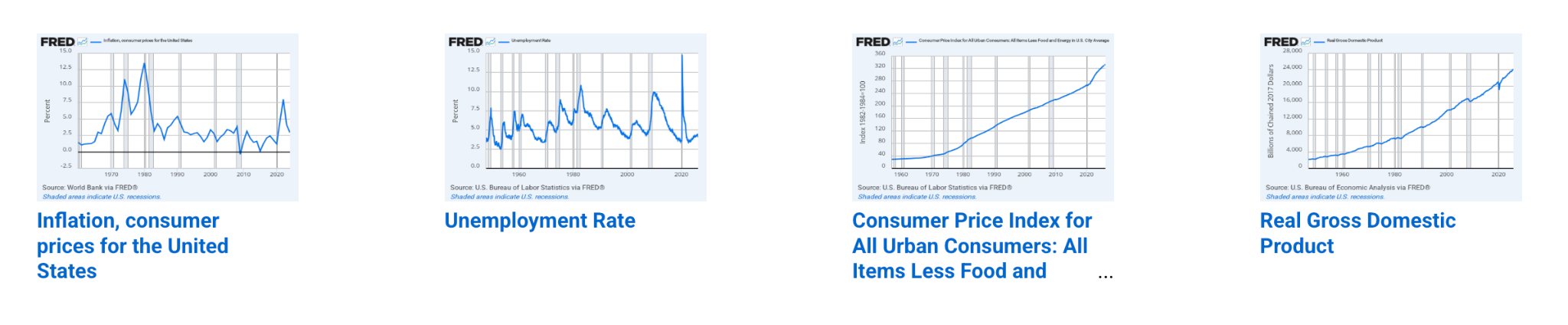

No single indicator captures inflation perfectly across an entire economy, which is why economists use several complementary indicators, each tracking causes of inflation from a different angle.

The Consumer Price Index (CPI) is the most widely cited. It tracks the cost of a fixed basket of goods and services – housing, food, transport, healthcare, clothing – weighted to reflect typical household spending. Because it directly measures what consumers pay, CPI is the standard reference for cost-of-living adjustments, wage negotiations, and benefit indexing.

The Producer Price Index (PPI) measures prices at the wholesale level – what producers receive for their output before it reaches consumers. Because production costs tend to flow downstream into retail prices with a lag, PPI is often used as a leading indicator of where CPI is headed.

The GDP deflator takes a broader view, measuring price changes across the entire economy rather than a fixed basket. Unlike CPI, it adjusts automatically for shifts in what people actually buy, making it useful for long-run comparisons but less practical for tracking current conditions.

The Personal Consumption Expenditures (PCE) price index is the Federal Reserve's preferred measure. It covers a wider range of spending than CPI, adjusts more flexibly for substitution behavior, and tends to run slightly lower than CPI as a result. When the Fed talks about its 2% inflation target, it is referring to PCE.

Taken together, these indicators help economists see what consumers are paying, how production costs are moving, and where broader price pressure is building.

Final take

Inflation is rarely the product of a single force. Demand surges, supply constraints, wage dynamics, monetary policy, and expectations interact in ways that make any one-cause explanation incomplete. The inflation of the early 2020s, for instance, combined pandemic-era supply disruption, aggressive fiscal stimulus, a labor market shock, and a decade of loose monetary policy – each factor amplifying the others.

That complexity makes inflation hard to manage and easy to misread. Identifying the inflation cause in any given episode requires looking at demand, supply, and expectations together – and recognizing that policy responses designed to address one driver can accelerate or dampen the others. At its core, inflation reflects imbalances across the broader economy. When that balance shifts, prices follow.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author