What is deflation and why it matters

Deflation is what happens when prices across an economy fall persistently over time. While cheaper goods might sound like a win for consumers, the reality is rarely that simple. Falling prices can discourage spending, depress wages, and push economies into prolonged stagnation – often with more lasting damage than inflation itself.

Deflation is a sustained decline in the general price level of goods and services across an economy. Unlike a temporary drop in prices for a single product or sector, deflation refers to a broad, persistent trend in which the purchasing power of money increases over time. Each unit of currency buys more than it did before.

Falling prices may sound like good news for consumers. But when deflation takes hold across an entire economy, the effects are far more complex and often damaging. Businesses face shrinking revenues as consumers delay purchases in anticipation of even lower prices. Wages come under pressure as companies cut costs. Investment slows. Unemployment rises. Debt also becomes harder to repay, because the real value of fixed loan obligations increases even as incomes fall.

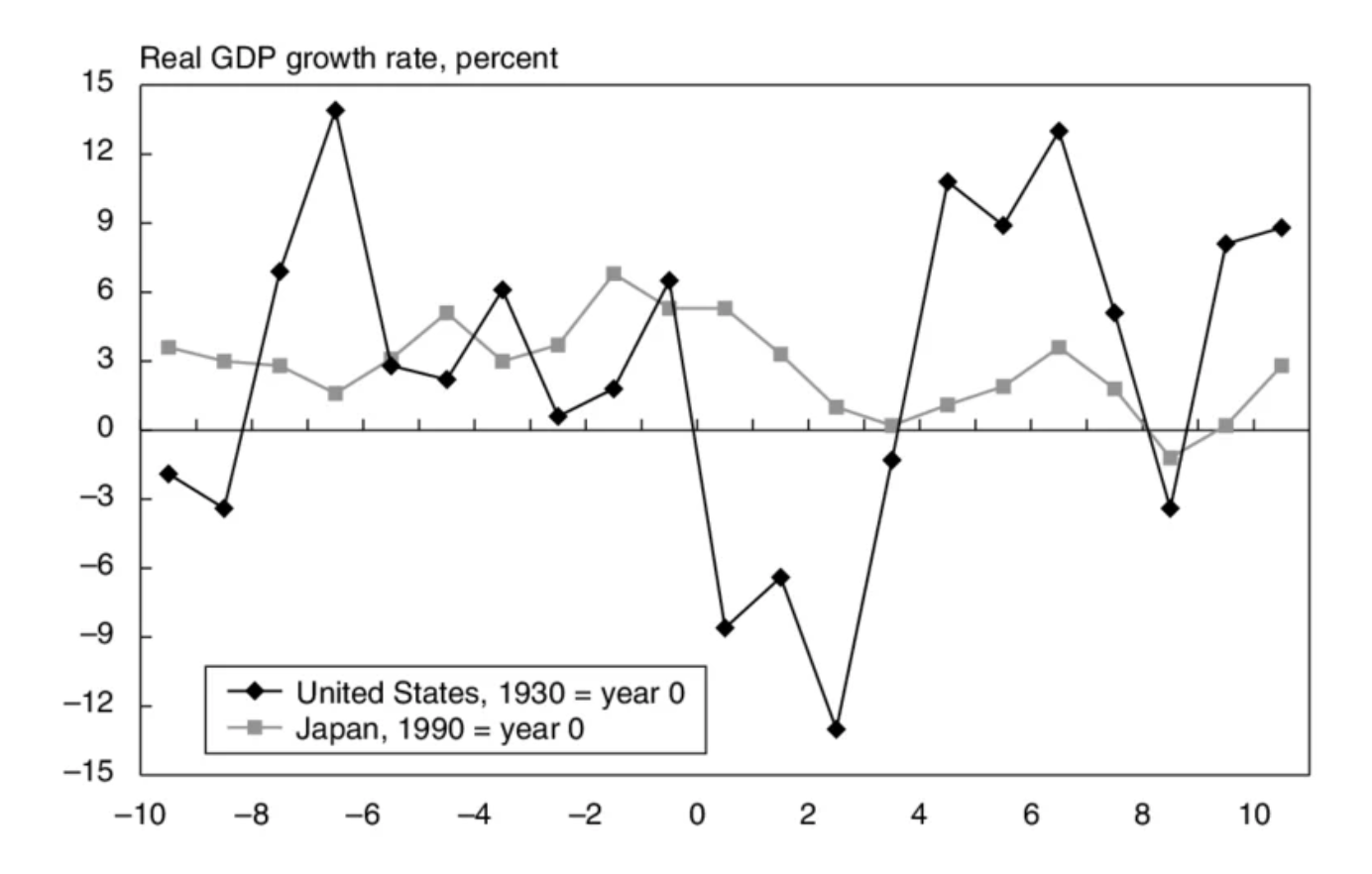

Deflation is closely associated with economic stagnation and recession. Japan's “Lost Decade” of the 1990s and the Great Depression of the 1930s are among the most studied examples of deflationary spirals, periods where falling prices and falling demand fed each other in a destructive loop. Recognizing deflation early matters because it becomes much harder to reverse once expectations adjust.

Main causes of deflation in the economy

What causes deflation? In most cases, several economic forces work together to reduce demand, restrict money supply, or expand supply beyond what the market can absorb.

Weak consumer demand is one of the most direct drivers. When households reduce spending due to job insecurity, falling wages, or rising debt burdens, businesses are forced to lower prices to attract buyers. If this decline in demand is widespread and sustained, it can push the entire price level downward.

Falling wages and unemployment compound the problem. As businesses face lower revenues, they cut costs by reducing headcount or wages, which in turn reduces consumer purchasing power further, creating a negative feedback loop.

A contraction in the money supply is another core cause. When central banks tighten monetary policy, or when credit markets freeze and lending declines, the amount of money circulating in the economy shrinks. With less money chasing the same amount of goods, prices fall.

Excess production capacity and technological advancement can also contribute. If supply grows faster than demand, whether due to automation, globalization, or overinvestment in production, prices are driven down. While technology-driven price declines in specific sectors are generally positive, economy-wide overproduction can tip into deflation.

Debt contraction and deleveraging play a particularly dangerous role. When households and businesses aggressively pay down debt rather than spend or invest, aggregate demand collapses. This was a defining feature of the 2008 financial crisis, when credit contraction threatened to push several major economies into deflation.

Recessionary pressure both causes and amplifies deflation. Economic contractions reduce output, employment, and income simultaneously, all of which suppress demand and put downward pressure on prices. This dynamic stands in sharp contrast to inflationary environments, where excess demand or supply shocks push prices upward. Readers looking to understand that side of the equation can explore what causes inflation in more detail.

How deflation is measured and identified

Measuring deflation is not simply a matter of watching prices fall. The harder part is separating a genuine, economy-wide deflationary trend from short-term price noise: a temporary dip in energy costs, a seasonal discount cycle, or a supply glut in one sector.

Economists approach this by looking at breadth, duration, and direction across multiple indicators simultaneously.

CPI is usually the first place analysts look. It reflects what consumers actually pay, and a sustained negative CPI reading is the clearest public signal of deflation. But CPI alone can mislead. Prices in some categories may fall while others rise, masking the underlying trend. This is why analysts disaggregate the index, looking for deflation spreading across core categories, particularly services, rather than being driven by volatile components like food or energy.

The GDP deflator broadens the picture. Because it covers the entire output of the economy rather than a fixed consumer basket, it can reveal deflationary pressure in sectors that CPI does not capture: business investment, government spending, exports. When both CPI and the GDP deflator move negative together, the signal becomes much harder to dismiss.

The PPI serves a different function in a deflationary context: it acts as a leading indicator. Falling producer prices often precede falling consumer prices by weeks or months, giving policymakers an early window to respond before deflation becomes entrenched.

The PCE, favored by the Federal Reserve, matters most at the policy level. Because it adjusts for substitution behavior and covers a broader spending universe than CPI, it gives central bankers a more stable read on where price trends are heading and whether a deflationary environment requires an aggressive monetary response.

Deflation becomes especially hard to identify in real time once expectations begin to shift. Once consumers and businesses begin to anticipate further price declines, they change behavior accordingly, delaying purchases and deferring investment, which reinforces the deflationary trend itself. By the time the indicators confirm it clearly, the spiral may already be underway.

Difference between inflation and deflation

The difference between inflation and deflation goes beyond a simple contrast between rising and falling prices. The two phenomena create fundamentally different incentive structures, and those differences shape how consumers spend, how businesses invest, and how debt functions across the economy.

Inflation means the general price level is rising. Each unit of currency buys less over time. While moderate inflation erodes purchasing power, it also encourages spending and investment, because consumers and businesses have an incentive to act now rather than wait. Borrowers benefit because the real value of their fixed debts decreases over time.

Deflation reverses this dynamic entirely. Higher purchasing power may sound appealing, but it creates powerful incentives to delay spending. Why buy today what will cost less tomorrow? This “paradox of thrift” can cause demand to collapse across the economy. Businesses respond by cutting production and jobs, which further depresses demand.

Deflation is also uniquely punishing for debtors. When prices fall, the real burden of debt increases. A borrower owes the same nominal amount, but that amount now represents a larger share of their income or assets. This debt deflation dynamic was central to the economic devastation of the 1930s.

This is why most central banks target a low but positive inflation rate, typically around 2% annually. A modest, predictable rate of inflation keeps the economy moving, maintains incentives to spend and invest, and provides a buffer against the deflationary trap.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author