Gold investment: is it actually worth it?

Gold has outperformed most asset classes in 2026 – but buying at all-time highs is a different question from whether gold belongs in a portfolio at all.

On this page

Few assets carry as much symbolism and baggage as gold. Central banks hoard it. Doomsday preppers bury it. Sophisticated fund managers quietly hold it alongside equities. The real question is whether any of that makes sense for an ordinary investor – or whether gold is often treated as a strategy when it is really just a habit.

Gold as an investment

Institutional investors hold gold primarily because it tends to move independently of stocks and bonds. Retail investors access it through physical bullion and coins, ETFs, mining stocks, and futures contracts, each with meaningfully different risk, cost, and liquidity characteristics.

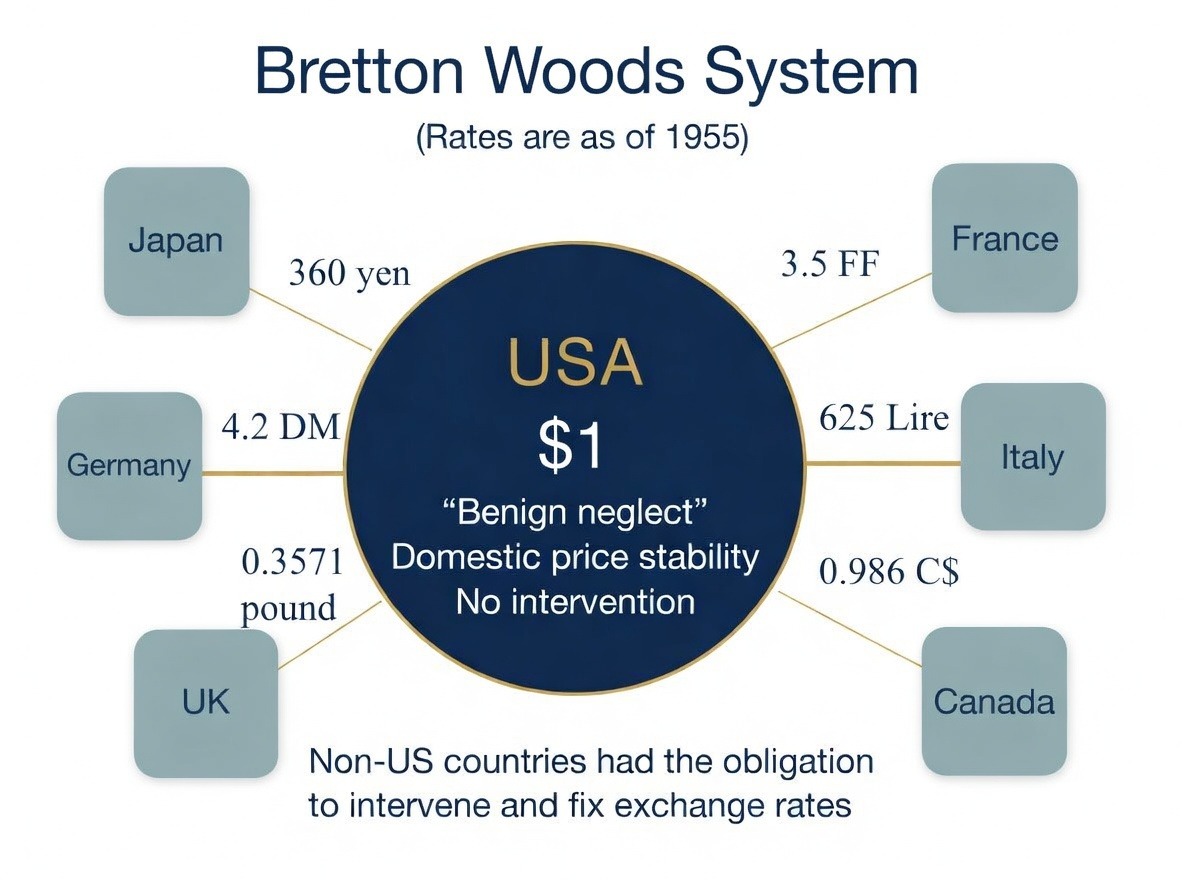

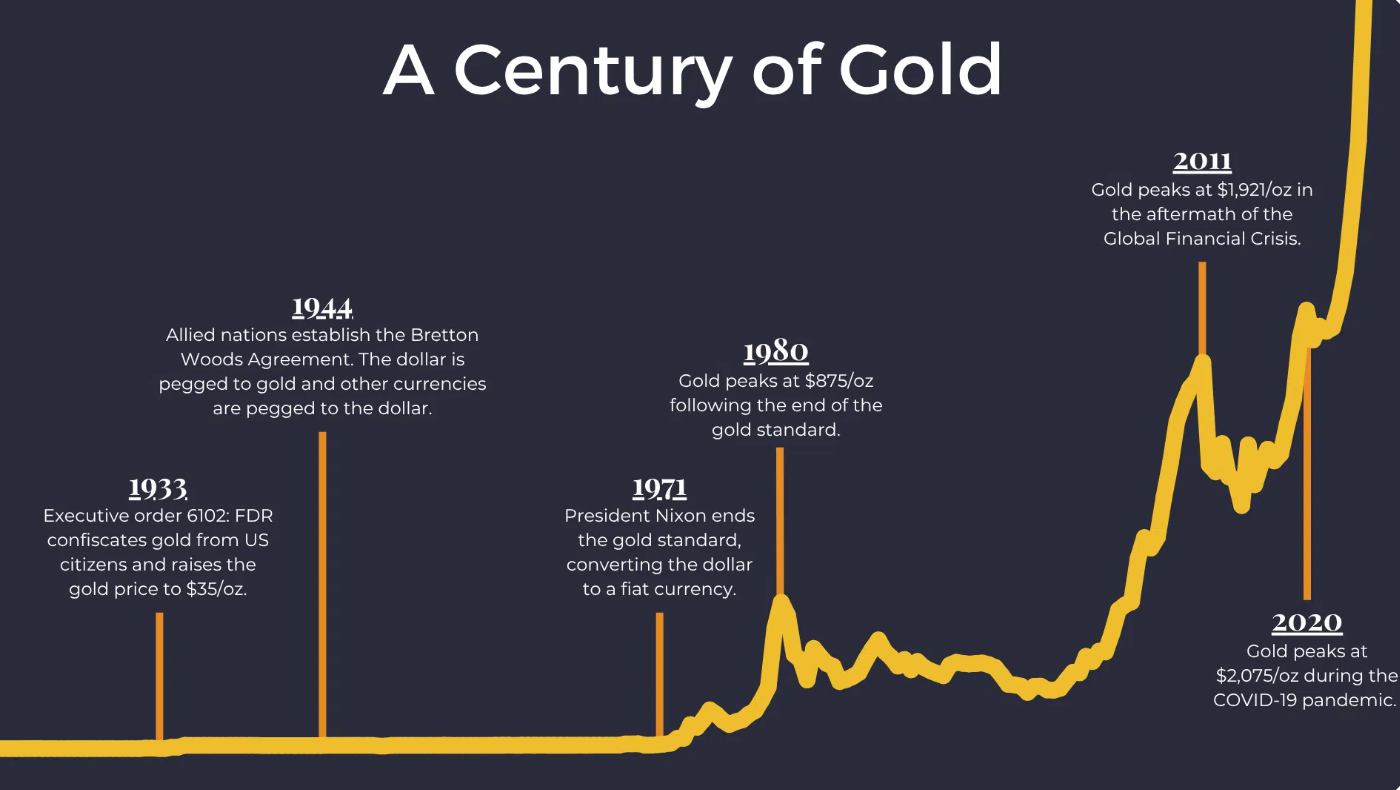

Gold's role in financial markets shifted dramatically in 1971 when the U.S. abandoned the Bretton Woods system and severed the dollar's link to gold. Before that, gold was a fixed anchor. After it, gold became a traded asset whose price is driven by sentiment, real interest rates, dollar strength, and geopolitical stress. That transition matters because since 1971, gold has had no cash flows. Its price is shaped by supply, demand, real rates, dollar strength, and broader risk sentiment.

Over very long time horizons, gold has done something remarkable: it has held its purchasing power. The common argument for gold is that it has preserved purchasing power across centuries far better than fiat money has. No fiat currency comes close to that record, which is why gold as an investment retains a logical place in portfolios even when it underperforms for years at a time.

Key advantages of investing in gold

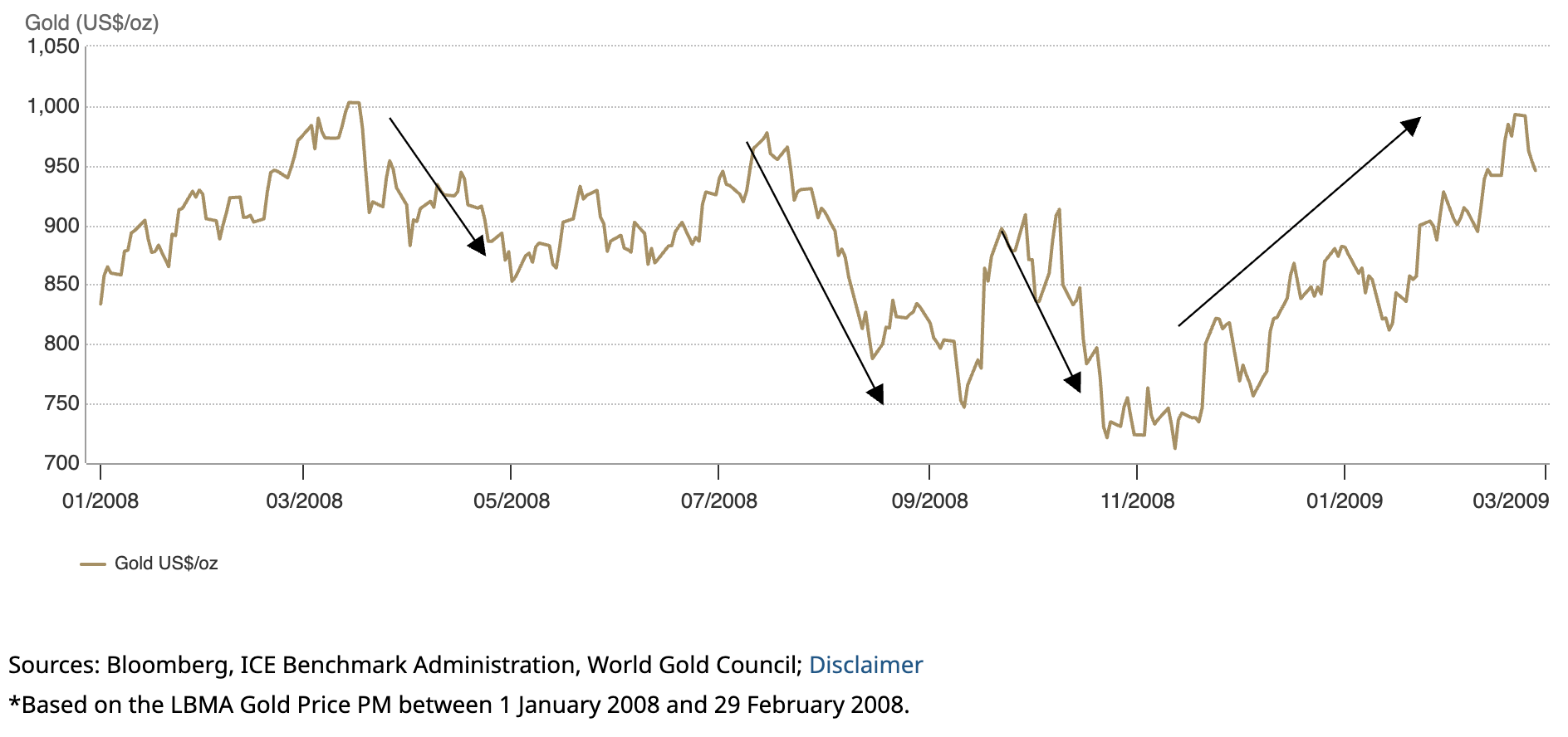

Is gold a good investment? A good place to start is with the conditions in which gold tends to perform well. Gold's correlation with equities is low or negative in most market environments, meaning it often rises precisely when stock portfolios are taking losses. During the 2008 financial crisis, gold gained roughly 25% while the S&P 500 fell close to 40%. During the COVID selloff in March 2020, it held its value while almost everything else collapsed. That is the main case for holding gold. Its value lies less in growing wealth and more in helping preserve it when other assets fail to do so.

Its inflation-hedging properties are real but less reliable over short periods than commonly assumed. Gold performed well during the high-inflation 1970s and again during the post-pandemic inflation surge of 2021 to 2024. Over decades, it tracks inflation reasonably well. Over a two- or three-year window, the relationship can break down entirely.

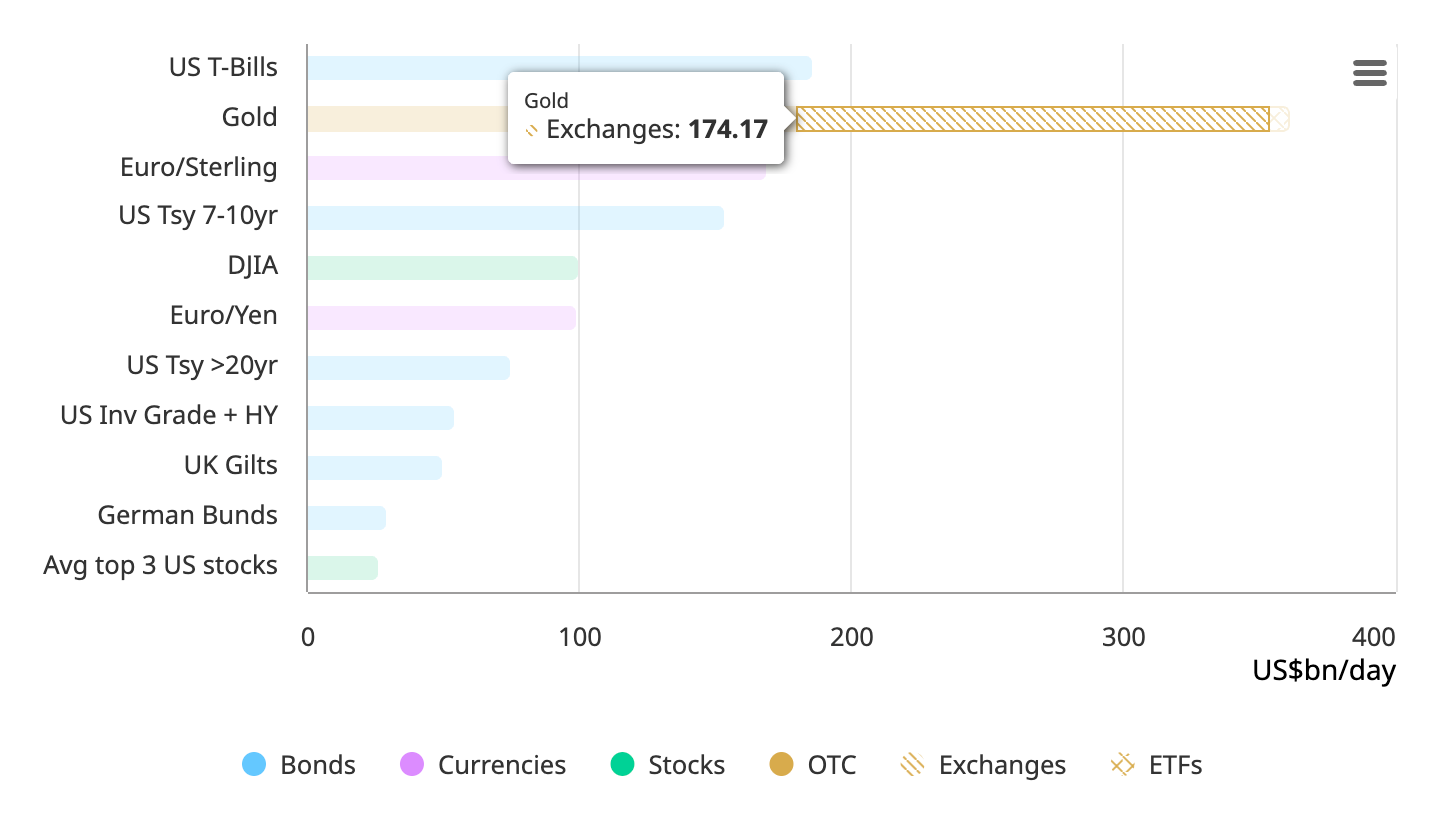

Liquidity is another advantage that often gets overlooked. The global gold market trades around $180 billion per day, more than most major stock exchanges. Selling a meaningful position in gold is straightforward in a way that liquidating real estate or private equity is not. And because gold carries no counterparty risk, it retains value even in scenarios where financial institutions fail – which is precisely the scenario some investors are trying to hedge against.

Potential drawbacks of gold investing

Gold investment has one built-in limitation: it produces nothing. A stock represents a claim on future earnings. A bond pays interest. Real estate generates rent. Gold simply holds its value over time, which means it has no compounding mechanism. Investors who hold it are not earning returns so much as preserving capital, and over long periods, that distinction costs real money.

The opportunity cost has been severe in certain eras. Between 1980 and 2005, gold lost value in real terms while equities compounded at extraordinary rates. Anyone who held gold through that period as a “safe” allocation gave up decades of growth. The 2011 peak is another example worth remembering: gold hit $1,900 per ounce and then fell more than 40% over the following four years. Investors who bought near that high waited until 2020 to break even. Gold is not a stable asset; it is an uncorrelated one. Those are very different things, especially in a bear market.

Physical ownership adds friction that erodes the appeal further. Storage costs, insurance, authentication on resale, and the spread between buying and selling prices all chip away at returns. Gold ETFs eliminate most of these problems but introduce ongoing management fees and, for some investors, a practical concern: an ETF is a paper claim on gold, not gold itself, which matters if the point was to hold something outside the financial system.

Is gold worth adding to your portfolio?

Is buying gold a good investment? A modest allocation – most advisors cite 5 to 10% – makes the most sense for investors who are concerned about prolonged inflation or currency debasement, who want genuine diversification beyond stocks and bonds, or who are in or near retirement and need to reduce the risk of a major drawdown at the wrong moment. In each of these scenarios, gold does a specific job that few other assets can replicate.

Gold is less compelling for younger investors with long time horizons who can ride out equity volatility, for those who need their investments to generate income, and for anyone expecting gold to compound meaningfully over decades. History is clear on this last point: equities have outperformed gold over virtually every 20- to 30-year period on record.

A 5 to 10% allocation to gold is a reasonable premium to pay for a portfolio that holds up better during financial crises, currency shocks, and sustained inflation. A portfolio built primarily around gold is a different bet entirely, and one that history has not rewarded.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author