Markets focus on earnings, central-bank meetings amid truce hopes

S&P 500 and Nasdaq hit intraday records Friday after reports of Pakistan-mediated U.S., Israeli and Iranian talks and a rally in Intel ahead of Fed, ECB and BoE meetings.

The S&P 500 and Nasdaq reached intraday records on Friday as reports of Pakistan-mediated talks involving U.S., Israeli and Iranian officials and a rally in Intel boosted risk appetite ahead of major central-bank meetings.

Reports indicated Iran’s foreign minister was traveling to Islamabad for talks and that U.S. envoys, including Jared Kushner, were set to join Pakistan-facilitated negotiations. Market participants treated the developments as a potential easing of tensions in the Middle East while still pricing the risk of ongoing energy disruptions.

The U.S. Dollar Index slipped 0.11% to 98.71 on Friday and remained on track for a roughly 0.5% gain for the week. EUR/USD recovered to about $1.1699 and the yen strengthened to around 159.62. Brent crude and U.S. West Texas Intermediate rose sharply this week, up about 16% and 11% respectively, after disruptions around the Strait of Hormuz tightened global supply.

Technology stocks led Friday’s gains. A jump in Intel shares helped lift the sector even as attention returned to a newly released AI model from a developer.

Corporate results have supported the market. More than 80% of S&P 500 companies that have reported so far have posted earnings above analysts’ estimates. Five of the largest U.S. tech firms are scheduled to report next week, representing a large share of the index’s market capitalization. The S&P 500 and Nasdaq were positioned for a fourth straight week of gains, the longest run since late 2024.

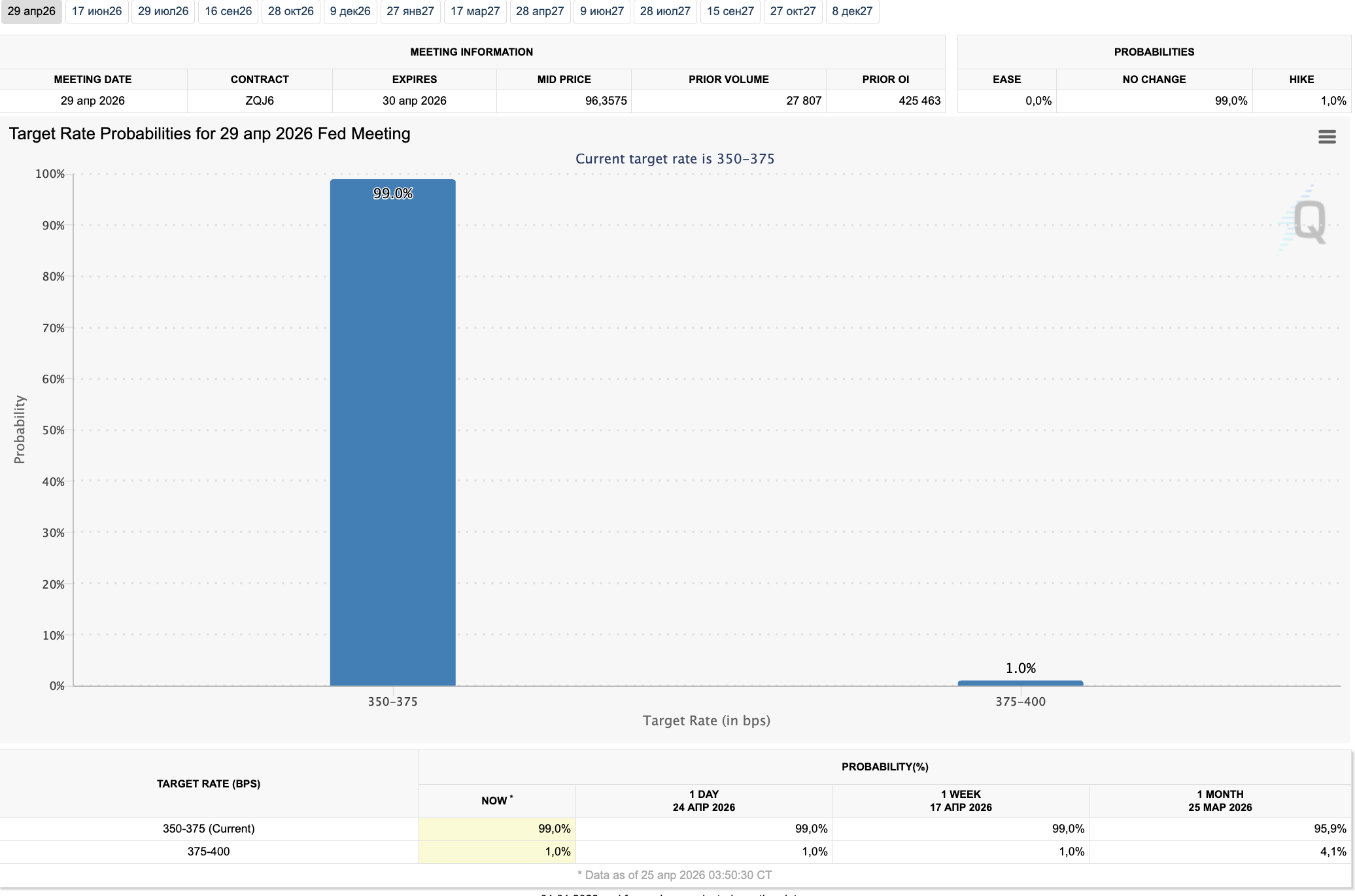

The Federal Reserve is widely expected to keep policy rates unchanged at its meeting on Wednesday, in what is scheduled as Chair Jerome Powell’s final planned meeting. Markets will watch Fed commentary for signals about the path to the committee’s decision in June. U.S. first-quarter GDP is forecast to rebound to about 2.7%, and the core personal consumption expenditures price index remains a key inflation measure for investors.

The European Central Bank and the Bank of England are also expected to hold rates at meetings on Thursday. ECB officials will receive new GDP and April inflation data ahead of their decision. In the U.K., officials are managing market expectations about future policy moves.

In Asia, the Bank of Japan is viewed as the wildcard for the week. Consensus forecasts expect no policy change, but Tokyo consumer prices have been rising and real interest rates remain deeply negative. China’s manufacturing purchasing managers index is due Thursday and is forecast near 49.9, a level that would signal a return to contraction. Australia’s consumer price index, due Wednesday, is projected to rise, in part driven by higher oil prices.

From a technical perspective, the U.S. Dollar Index is testing a turning point after a recovery from January lows, with near-term resistance around 99.56 and support near the 100- and 200-day moving average cluster close to 98.50.

Traders said central-bank commentary and a heavy slate of economic data and earnings reports will guide market moves in the coming days.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author