Germany moves to tighten crypto tax reporting under DAC8

Starting in 2026, exchanges serving German users must report customer and transaction data under EU DAC8, while tax offices expand tools to tie blockchain activity to taxpayers.

Germany is tightening oversight of crypto taxes under the European Union’s DAC8, which took effect in the country on Jan. 1. Beginning in 2026, crypto-asset service providers that serve German residents must collect and transmit standardized customer and transaction data to federal and state tax administrations to curb tax fraud and improve transparency.

The directive sets up automatic exchange of information on crypto asset flows among EU member states. The rules apply to firms based in Germany and companies abroad that offer services to German users, including platforms such as Binance exchange, Bitpanda, Bison, Kraken or KuCoin.

Tax offices are expanding expertise and rolling out software to link blockchain activity to individuals. Authorities are using tools from blockchain analytics vendors, including Chainalysis, to associate wallets with taxpayers and to check reported gains and losses.

The reporting requirements increase the need for complete records. Investors who have used multiple exchanges or moved coins between wallets may need to reconstruct their transaction history to calculate gains. Conversions between cryptocurrencies and the use of digital assets for payments can be taxable events.

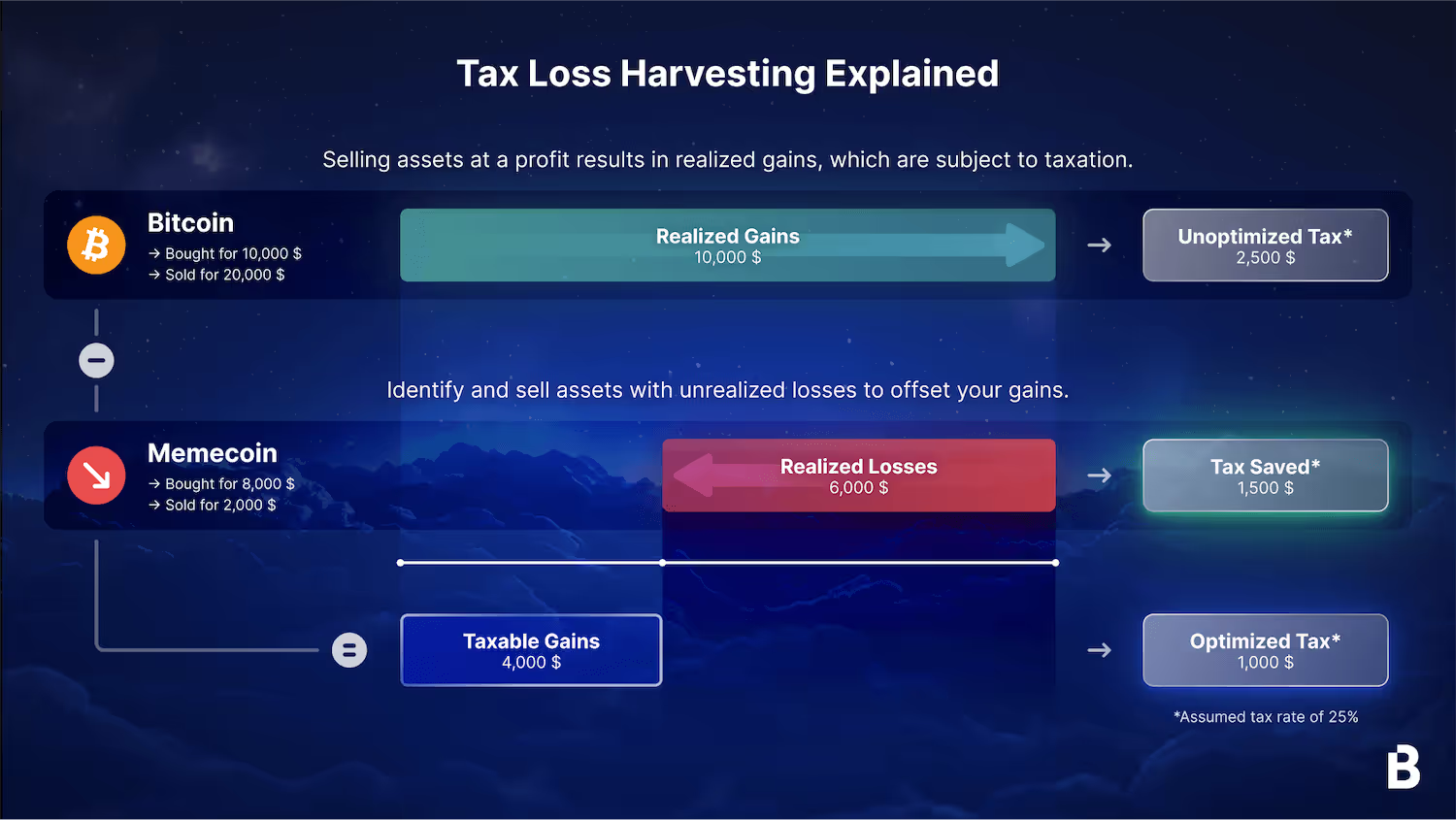

In Germany, Bitcoin and other digital assets are treated as private assets. Profits from private sales are tax-free up to €1,000 per year. Gains on coins held for more than one year are exempt from tax. Income from staking, lending or mining is tax-free up to €256 annually. If these thresholds are exceeded, the entire amount becomes taxable. Taxable crypto gains are subject to the progressive personal income tax, which ranges from 0% to 45% based on total income. When income tax due exceeds €18,130, a solidarity surcharge of up to 5.5% of the tax applies. Losses from crypto transactions can be offset against profits from other private disposal transactions.

| Taxable income range for single taxpayers (EUR) | Taxable income range for married taxpayers (EUR) | Tax rate (%) | ||

| Over | Not over | Over | Not over | |

| 0 | 12,096 | 0 | 24,192 | 0 |

| 12,096 | 68,429 | 24,192 | 136,858 | 14 to 42* |

| 68,430 | 277,825 | 136,860 | 555,650 | 42 |

| 277,826 | and above | 555,652 | and above | 45 |

Tax returns for the 2025 tax year are due by the end of July 2026. Data sharing under DAC8 is set to begin in 2026 across Germany and the wider EU.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author