Curve founder proposes market model for DeFi bad debt

Michael Egorov proposes converting nonperforming DeFi loans into tradable claims sold to investors to set market prices and limit lender losses after the KelpDAO fallout.

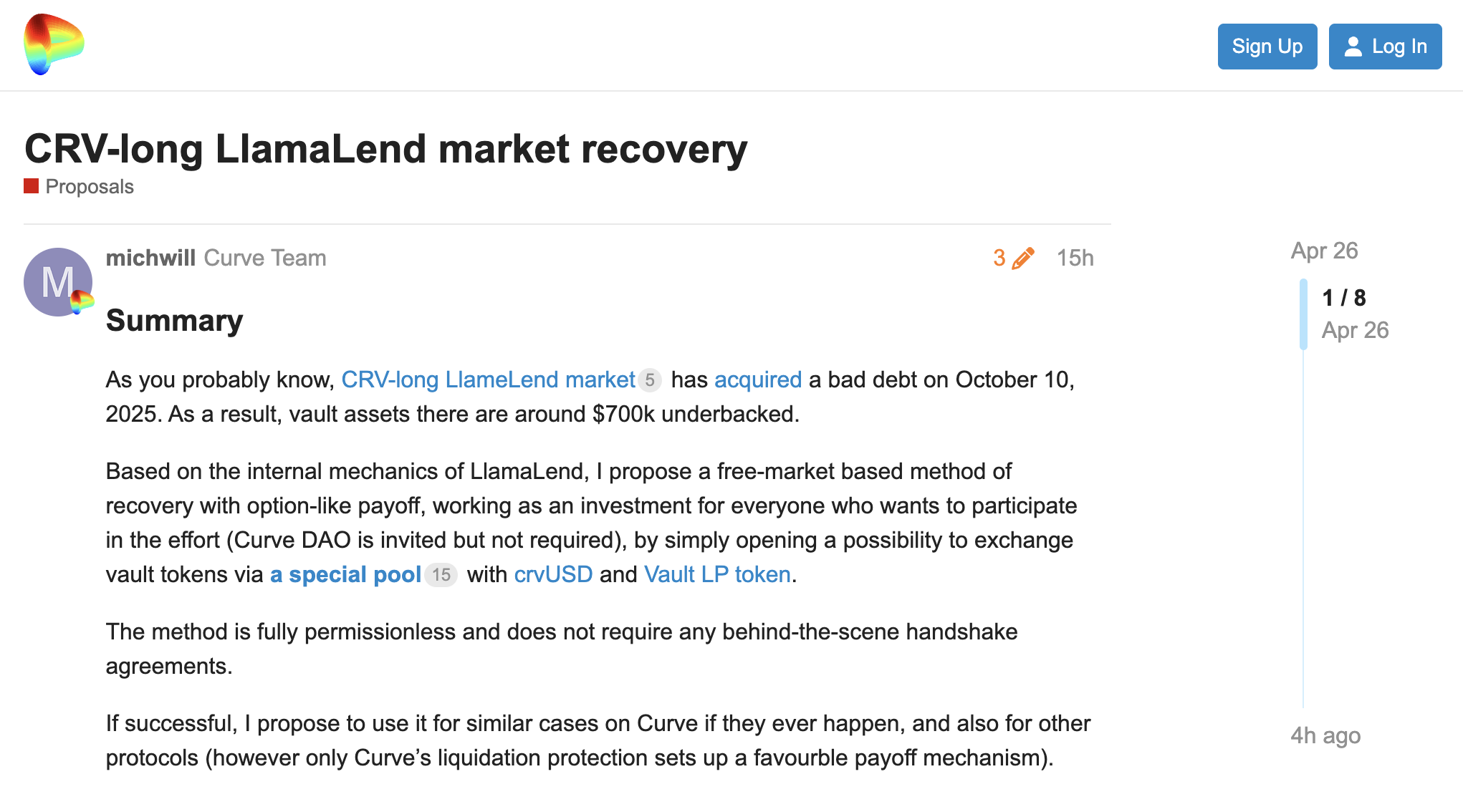

Curve founder Michael Egorov proposed a market-based model to recover bad debt in decentralized finance lending in a community proposal shared with Curve governance and other DeFi participants.

The proposal calls for tokenizing delinquent loan positions into transferable bad-debt tokens that can be sold to third-party investors through open auctions or structured tranches. The aim is to create on-chain price discovery for distressed credit and channel recovered value back to the original lending liqudity pool.

Under the plan, loans that enter default or become undercollateralized would be packaged as transferable tokens. These tokens could be auctioned publicly, split into senior and junior tranches to match different risk appetites, or sold to specialized market makers. Proceeds from sales would be distributed to affected lenders in proportion to their exposure, with sale prices providing a transparent market valuation for the impaired assets. The proposal includes support measures such as minimum reserve prices, time-limited auctions and oracle-based price feeds to guide bids and protect sellers.

Supporters argue the mechanism would allow external capital to price and assume distressed assets instead of relying on protocol write-downs or governance-funded recapitalizations. The framework is presented as usable for a single large default or as a recurring tool to manage occasional nonperforming loans.

Responses from governance members, developers and other DeFi participants were mixed. Some welcomed the focus on market pricing and transparency. Others raised concerns about operational complexity, the risk of front-running in auctions, manipulation by coordinated buyers, the availability of sufficient risk-tolerant capital, how oracles would supply reliable valuations and legal implications for buyers in different jurisdictions.

The proposal follows the KelpDAO incident, which left a set of on-chain loans classified as nonperforming and prompted debate about how to handle losses that arise without clear off-chain counterparties.

If Curve governance approves a pilot, next steps would include specifying the tokenization format, auction mechanics and safeguards against manipulation, and coordinating with other lending protocols that might adopt the mechanism. Pilot auctions would likely begin with smaller, well-understood positions to test market appetite and execution before moving to larger cases.

DeFi lending platforms use collateralized loans and automatic liquidation to manage credit risk. When liquidations fail or collateral values fall faster than liquidations can execute, loans can become undercollateralized and create bad debt. Past recovery options have included on-chain collateral auctions, governance-funded recapitalizations and socialized losses. The model proposed by Egorov would add an option to transfer distressed on-chain credit to third-party buyers through open-market pricing.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author