3 things Goldman Sachs wants you to know about the stablecoins

Goldman Sachs, one of the biggest U.S. banks, labels Summer 2025 as a season of stablecoins, highlighting the biggest developments in the sector.

As summer 2025 draws to a close, Goldman Sachs released a report calling the period “Stablecoin Summer.” The bank highlighted developments in the sector, including the GENIUS Act in the US, major companies exploring their own stablecoins, and the public listing of USDC issuer Circle. Goldman Sachs also examined the potential implications of stablecoins for banks and included insights from economists and financial market experts. Next, we’ll take a closer look at three key takeaways from the report.

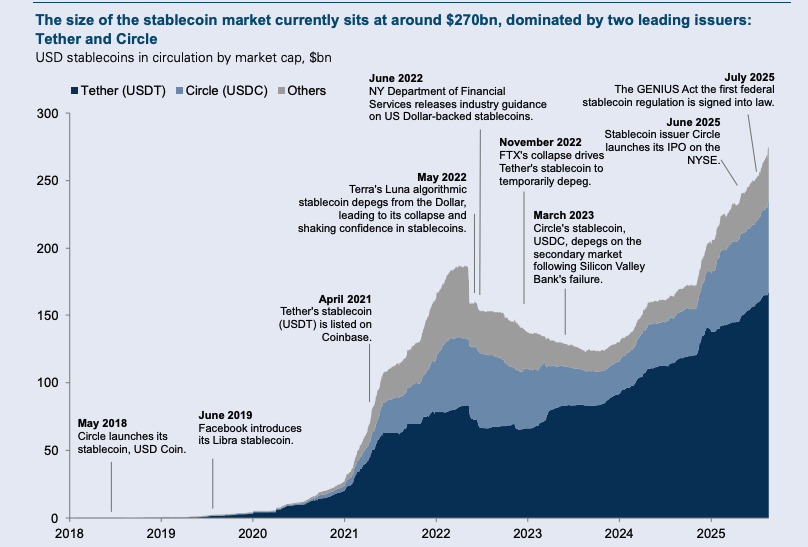

Global stablecoin market estimated at $270B

Goldman Sachs mentioned the substantial growth of the stablecoin market in recent years and its current size of $270 billion. According to the bank, they have gained traction for use cases like cross-border transfers and as a tool to access dollars outside of the US. The majority of stablecoins are pegged to the US dollar, with USDT and USDC being the largest ones.

Summer 2025 proved particularly eventful for stablecoins. On July 18, President Donald Trump signed the GENIUS Act into law, which is the first-ever federal regulatory system for stablecoins. Earlier, on June 5, Circle went public on the NYSE. At the same time, major companies like Walmart and Amazon are exploring the launch of their stablecoins. Given the bullish movement, stablecoins are expected to continue growing.

Brian Brooks, a former Acting Comptroller of the Currency and current Chairman and CEO of Meridian Capital Group and board member of Strategy, says that among the key drivers for stablecoin adoption is the huge demand for dollars globally, and stablecoins are representations of the USD.

The GENIUS Act will unleash demand for the dollar at unprecedented levels,” Brooks predicted, adding, “I expect the future state to become reality in two years and exist at scale in five years. So, the next three years will be the gold rush.

Potential effects of stablecoins on financial stability

The GENIUS Act and its possible implications have been a hot topic of discussion, with banking groups debating stablecoin’s yield generation options. Although the framework explicitly bans permitted payment stablecoin issuers from paying any form of interest or yield to holders, critics say there are still loopholes in the law. The Goldman Sachs report analyzes of stablecoins on financial stability. Brian Brooks believes that the GENIUS Act creates a sense of safety around stablecoin usage and prevents low-cost deposits from being taken away from community banks. According to him, while there are some challenges in supervision, regulators are taking steps to catch up with the technology. On the other hand, Barry Eichengreen, Professor at the University of California, Berkeley, said stablecoins can disrupt economic stability.

My main concern is that the proliferation of stablecoins could undermine what economists refer to as the “singleness of money” – the principle that every dollar should trade at the same price and be accepted everywhere – which is essential for economic stability

Eichengreen said.

Eichengreen is concerned that the GENIUS Act could create many different currencies and stablecoin-like tokens that don’t work well together and may have different values. Goldman Sachs researchers predict that the spread of stablecoins will result in increased demand for safe assets, including Treasury bills. However, there are risks that stablecoins may make managing U.S. debt more difficult and eventually lead to higher borrowing costs.

Goldman Sachs’ Take on Bank-Blockchain Collaborations

Currently, stablecoins are mostly used for crypto trading and for accessing U.S. dollars outside the country. But Goldman Sachs points out that tokenization – turning real-world assets into digital tokens on a blockchain – could give them a bigger role. The market for tokenized assets is still small at about $295 billion, and most of that is in stablecoins. But the potential is huge. For example, the U.S. mortgage market is worth $13 trillion, yet it’s slow and full of paperwork. Putting mortgages on blockchain could cut costs and make settlement faster.

According to Goldman Sachs, broader tokenization of the U.S. economy is the most obvious bull case for stablecoins disintermediating banks. If goods and services are exchanged on blockchains with tokenized dollars, stablecoins could take the place of some bank deposits.

However, the bank notes that the industry is still in its early stages. Banks have also started to issue their own digital currencies, which could compete with stablecoins and potentially limit their impact on bank deposits. JP Morgan, for example, launched a deposit token in partnership with Base. In the future, Goldman Sachs expects increased collaboration between banks and blockchain companies.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author