Generation Wallet: Deutsche Bank Maps Tokenized Wealth Transfer

Deutsche Bank and Baker McKenzie warn that the $84T wealth shift from Boomers to Gen Z could reshape finance—if tokenization avoids legal limbo and gains real traction.

The largest wealth transfer in history is more than a financial event; it represents a generational software update. According to Deutsche Bank, $84 trillion will shift from Baby Boomers to Millennials and Gen Z by 2045.

But if you expect those trillions to quietly enter brokerage accounts or sit in treasuries, think again. This isn’t just a story about inheritance—it’s about infrastructure.

And the platform of choice? Blockchain.

A new whitepaper, a collaboration between Deutsche Bank and Baker McKenzie titled ‘Tokenization of Financial Markets: Mapping the Plausible Future through Scenario Analysis,' unequivocally states: tokenization isn’t a “what if,” it’s a “when.”

More precisely, it’s a “how soon,” and the answer might be closer than you think.

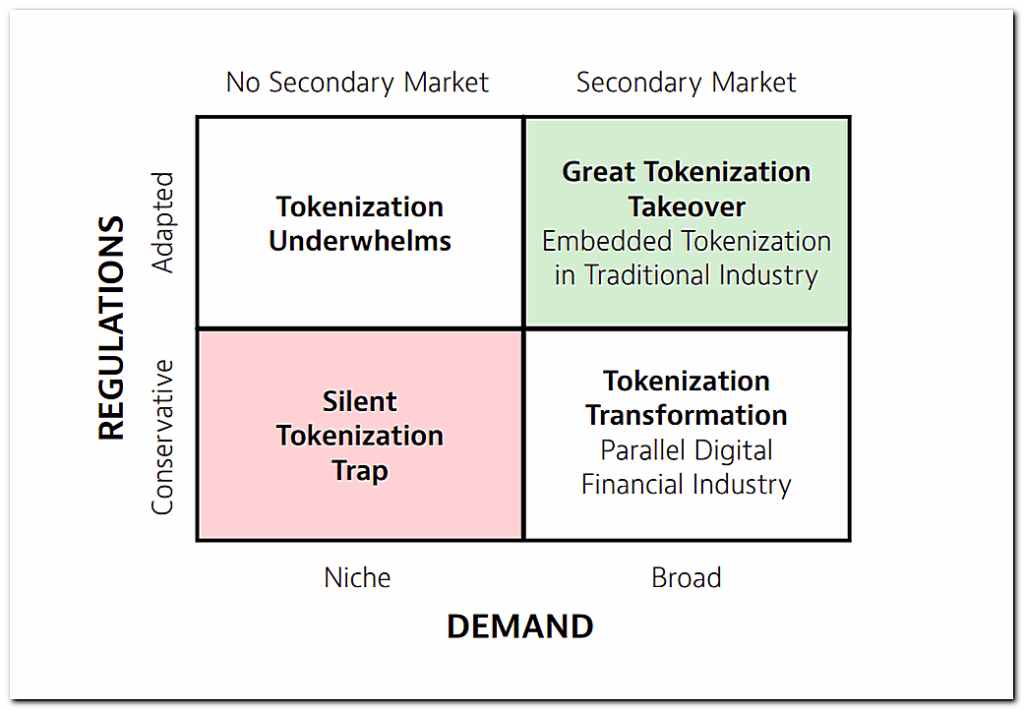

The Coming Fork: Takeover or Trap?

The report outlines two divergent futures for tokenization.

- The optimistic ‘Great Tokenization Takeover'

Envisions digital assets deeply integrated across global capital markets, encompassing everything from sovereign bonds to real estate and private equity.

- The more cautious ‘Silent Tokenization Trap'

Depicts innovation languishing in isolated trials, hampered by regulatory uncertainty, market fragmentation, and insufficient secondary market liquidity.

This binary is more than theoretical. It’s directional. And the deciding factor may not be code or custody—it may be culture.

The Millennial Catalyst

The report identifies generational change as the key catalyst. Notably, Millennials and Gen Z are five times more inclined to hold digital assets compared to Baby Boomers. As this $84 trillion transitions hands, it doesn’t just enter new wallets—it enters new worldviews.

This generation grew up with:

- mobile banking,

- borderless commerce,

- 24/7 everything.

They’re not looking for PDFs and paper shares—they expect:

- programmable assets,

- instant settlement,

- tokenized ownership over funds, homes, startups, and beyond.

In emerging markets like India and Vietnam, digital asset adoption is soaring. The reasons aren’t ideological—they’re infrastructural. In countries where traditional finance remains limited or extractive, tokenization isn’t just better. It’s available.

This is the latent demand the report outlines: a new generation with capital and expectations incompatible with old rails.

From Experiment to Emergence: A Timeline of Tokenization

One of the most compelling features of the report is a chart that tracks key milestones in tokenized finance from 2018 to 2024—an image widely circulated in crypto circles, including a tweet from @GenfinityIO that’s since gone viral.

The chart reveals a progression from concept to implementation:

- 2018–2020 (Innovation): stablecoins on Ethereum, tokenized deposits, first legal recognitions.

- 2021–2022 (Emergence): cross-border fund launches on Polygon, tokenized MMFs on Stellar.

- 2023–2024 (Post-Pilot Maturity):

- Cross-chain repo deals,

- Regulatory guidance from MAS and HKMA,

- Sovereign-grade digital bonds,

- Deutsche Bank’s Project DAMA 2, launched as a multi-chain MVP on Ethereum.

The right edge of the chart forecasts the next 2–3 years: tokenized asset management, composable funds, round-the-clock redemption—all fully integrated across chains and geographies.

The message is unmistakable: we are no longer theorizing about tokenization. We are living in its early implementation. And we’re two steps from the mainstream.

The Bottleneck: Secondary Markets

So what’s holding it back?

- Liquidity.

- Secondary trading.

- Market structure.

While primary token issuance is surging—MMFs, debt products, equity funds—secondary markets remain dangerously underdeveloped. Without real-time trading, pricing mechanisms, or market makers, these digital assets sit in digital vaults, waiting to be useful.

The report notes that even the most progressive jurisdictions (like Switzerland and Hong Kong) are still building the regulatory and technological bridges required for tokenized assets to circulate at scale. Basel III capital requirements still deter traditional banks from market-making. This opens a window for fintechs—but only if they can fill the liquidity vacuum responsibly.

It’s not a tech problem. It’s a trust problem.

TradFi or Web3? Choose Your Fighter

Another powerful theme in the report is the question of architecture: should tokenization run parallel to traditional finance or become embedded within it?

The parallel model envisions fintechs and NBFIs leading the way—launching tokenized funds, operating decentralized platforms, and building new infrastructure without the baggage of legacy compliance.

The embedded model, by contrast, calls for banks and Web3 to work together under updated regulation.

Here, tokenized assets are treated like any other collateral:

- bankable,

- reportable,

- institutionally safe.

The report suggests that a hybrid model is most plausible. Fintechs bring speed and innovation; banks bring credibility and capital. One without the other, and tokenization remains niche.

The Regulatory Crossroads

Regulation is the final boss.

To unlock demand, regulators must provide legal certainty—treating on-chain records as valid proof of ownership, allowing for cross-border alignment, and harmonizing investor protections.

To unlock supply, they must clarify tax treatment, streamline classifications, and create a framework that doesn’t penalize innovation.

The report points to critical uncertainties:

- What happens when a token crosses chains?

- Can tokens be used as repo collateral?

- Are digital assets subject to stamp duty?

Deutsche Bank and Baker McKenzie don’t offer final answers—but they argue that unless governments move quickly, the tokenization takeover could stall in legal purgatory.

When Infrastructure Meets Inheritance

Here’s the punchline: this isn’t about tokens. It’s about timing.

Tokenization’s potential doesn’t live in code—it lives in coordination. As trillions migrate to a digitally native generation, the infrastructure must catch up—or risk irrelevance. Every month of regulatory indecision or fragmented standards pushes adoption further from inevitability and closer to impossibility.

Deutsche Bank believes we have 2–3 years to get it right.

That’s not a lot of time.

But it might be just enough.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author