AI data centers may reshape US grid, emissions and rates

US data centers could use 14% of power by 2030 and 18% by 2035, lifting total grid costs 13%–15% and shifting 2035 rates: commercial −3%, residential +2%, an energy outlook finds.

A new analysis by Rhodium Group finds that accelerating AI adoption could push US data centers to consume 14% of national electricity by 2030 and 18% by 2035 — lifting total grid costs by 13%–15% and shifting rates unevenly: commercial customers could see bills fall about 3%, while residential rates rise around 2%.

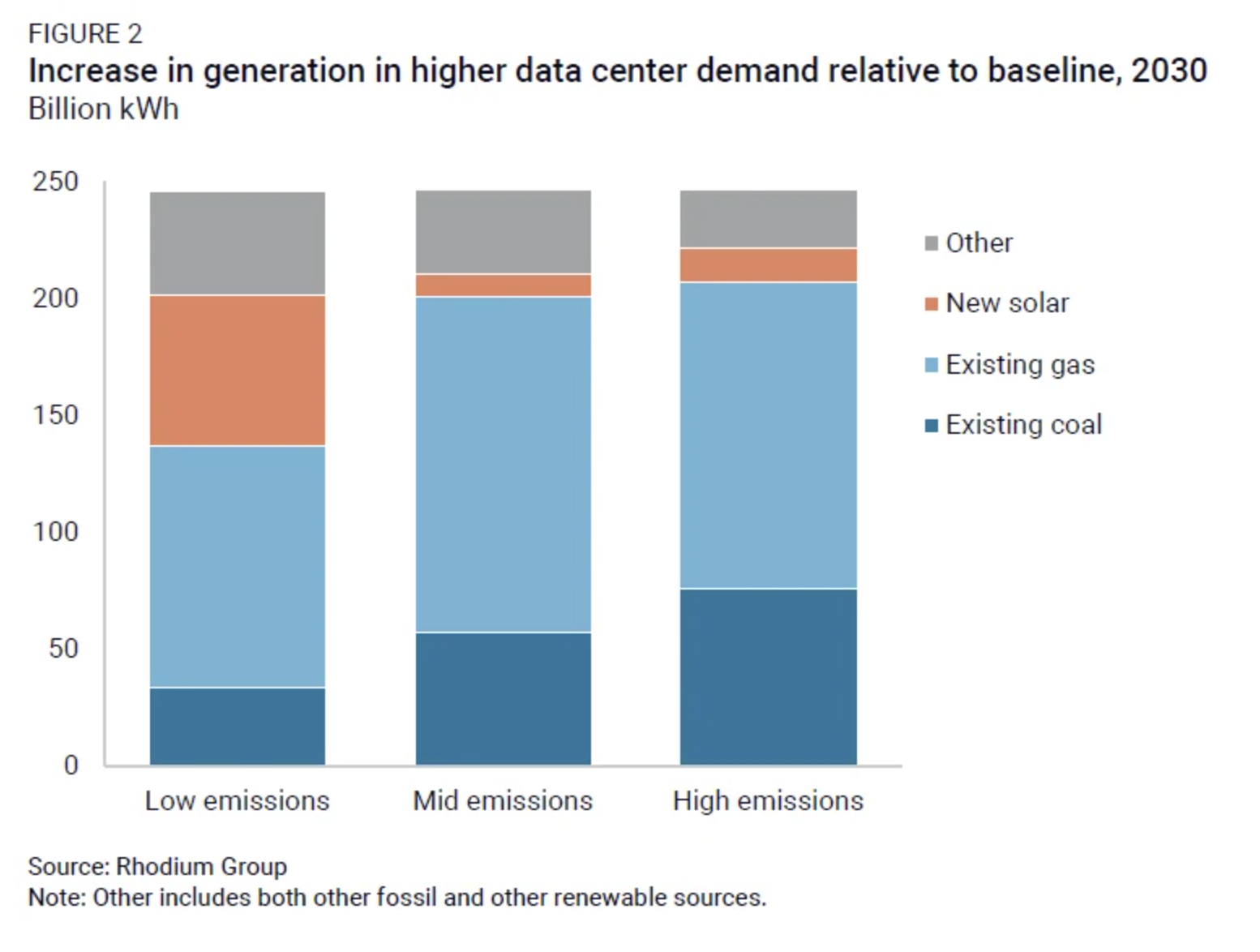

The scenario applies a 30% faster annual growth rate for data center demand through 2030 and 25% faster through 2035, reflecting rapid AI adoption and ongoing buildouts. With supply chains tight, interconnection queues long, and permitting slow, the study finds little room to add much new generation before 2030. In the near term, existing gas and coal plants run more to cover higher loads, meeting an estimated 55% to 85% of extra demand relative to the baseline.

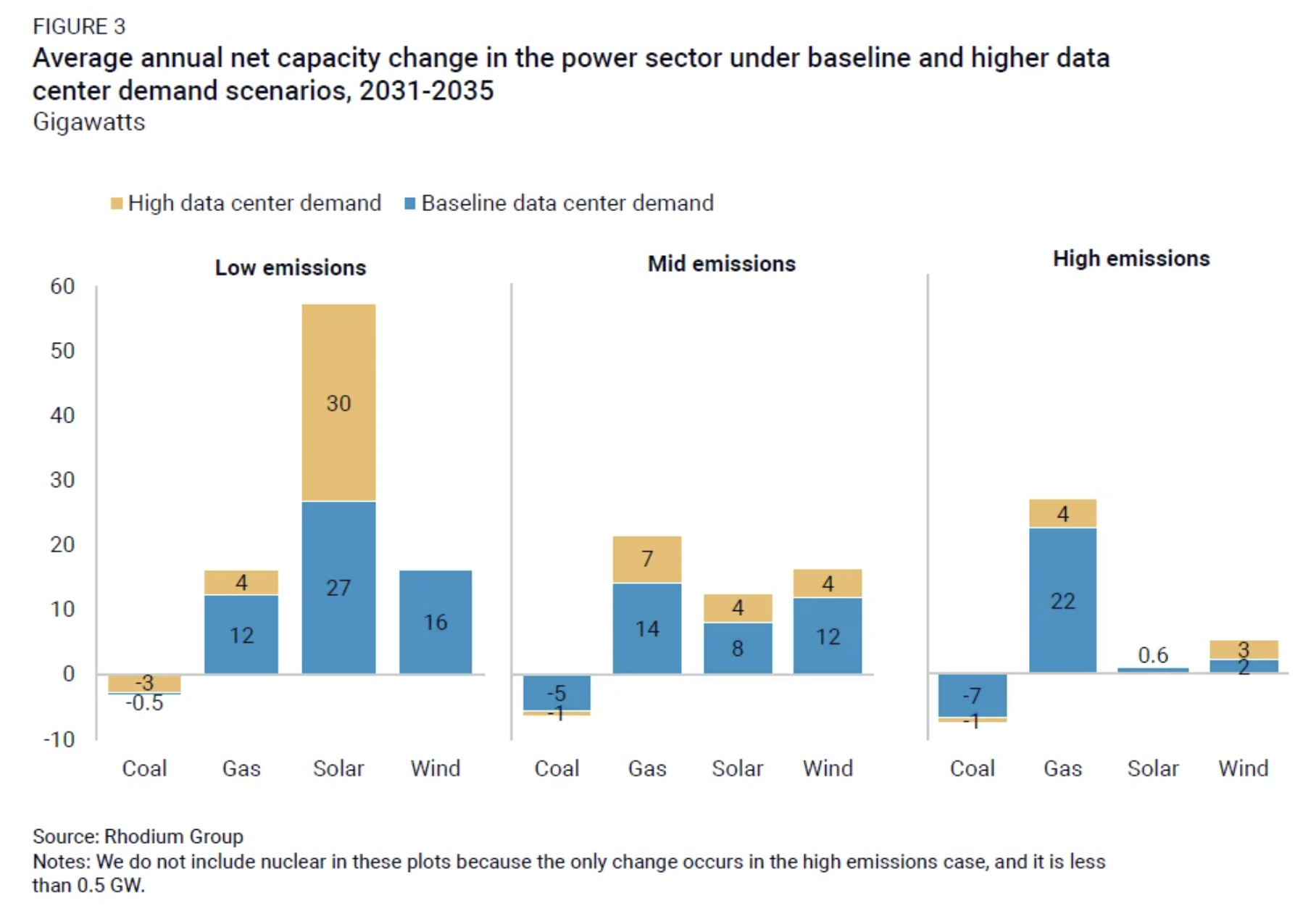

By 2035, the grid response depends on market conditions. In a low-emissions case marked by cheaper clean technologies and higher fossil fuel prices, solar and wind dominate additions, and higher data center demand amplifies that trend, with new solar builds more than doubling versus the baseline. In a high-emissions case with inexpensive gas and slower clean cost declines, gas capacity makes up most additions and sector emissions rise compared with the baseline, though corporate clean power purchases could offset part of the increase.

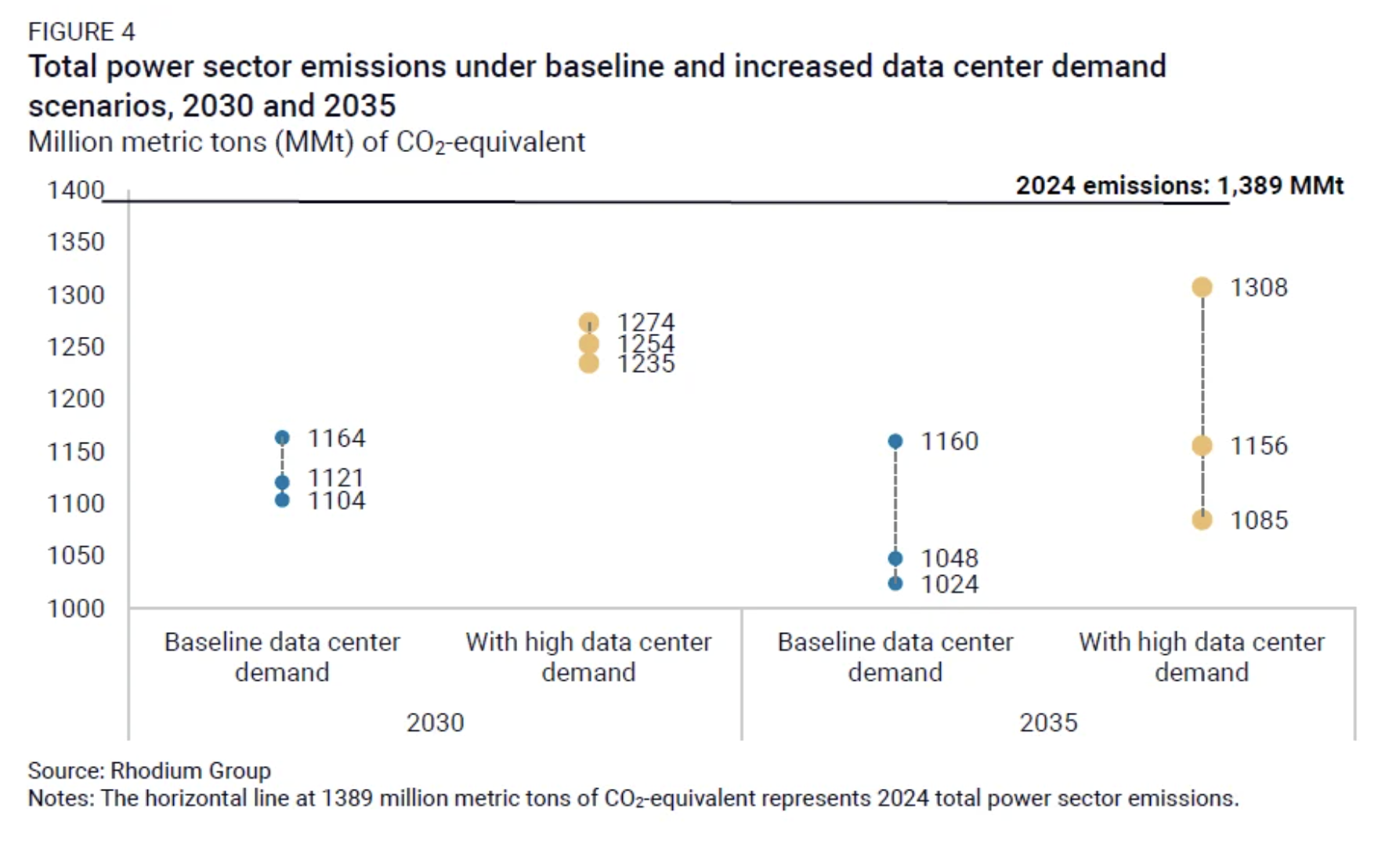

Under current policy, total power-sector emissions decline this decade. The outlook shows a 17% to 21% drop below 2024 levels by 2030. In 2035, emissions fall 25% to 27% below 2024 in the low- and mid-emissions cases, while the high-emissions case holds near 17% below. With higher data center demand, 2035 emissions land 6% to 13% above the baseline yet remain 6% to 22% under 2024 levels.

Rising demand lifts system costs, even if average rates stay steady. The study estimates a 13% to 15% increase in total system costs by 2035 under higher data center demand. Commercial customers benefit because large new loads expand total sales, while residential usage changes little, pushing household rates slightly higher. These shifts would come on top of recent retail increases that have run ahead of inflation, driven by disaster recovery spending, higher equipment costs, and expected new demand.

How to assign costs for new supply and grid upgrades is under debate. Proposals include having large data centers pay the full energy costs linked to their new builds in some markets, and a Rate Payer Protection Pledge backed by the Trump administration that would place the costs of new capacity and grid enhancements on developers. Even with such measures, strong demand for turbines, transformers, and other equipment could lift project costs unless siting, permitting, and interconnection timelines improve and manufacturing expands.

The report highlights wide uncertainty around future data center electricity needs. The gap between the lowest and highest 2030 projections exceeds the current combined electricity use of California and Florida. Methods differ, from interconnection queues that often overstate eventual load to hardware shipment tracking, and newer forecasts tend to be higher. One recent update lifted a 2030 data center load estimate by 55% to 65% compared with a 2024 outlook.

Corporate power buying could moderate emissions. Companies procured about 130 GW of clean power from 2014 through 2025, equal to at least 4% of US generation. Many hyperscale operators hold clean energy commitments, and federal researchers estimate roughly half of data center growth through 2028 will come from these firms. Some of the clean capacity expected over the next decade likely reflects data center purchases. Longer-term investments by hyperscalers in advanced nuclear, geothermal, and carbon capture may also affect the grid, though the timing and scale are uncertain.

Taking Stock 2025 models outcomes under current federal and state policies and typical market conditions. The authors note that recent trade actions and efforts by the Trump administration to slow wind and solar development have not matched stable market conditions for clean technologies, adding uncertainty to how the power mix and prices will evolve with rising data center demand.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author