Tesla Q1: AI, robotaxis versus slipping auto margins

Tesla reports Q1 2026 on April 22 after the close. Investors will watch if FSD, Optimus and robotaxi spending tied to over $20 billion in CapEx can offset missed deliveries and weaker auto margins.

Tesla will report first-quarter 2026 results on April 22 after the market close. Investors will watch whether revenue from Full Self-Driving software, the Optimus humanoid robot and a planned robotaxi network can offset a shortfall in deliveries and pressure on automotive margins.

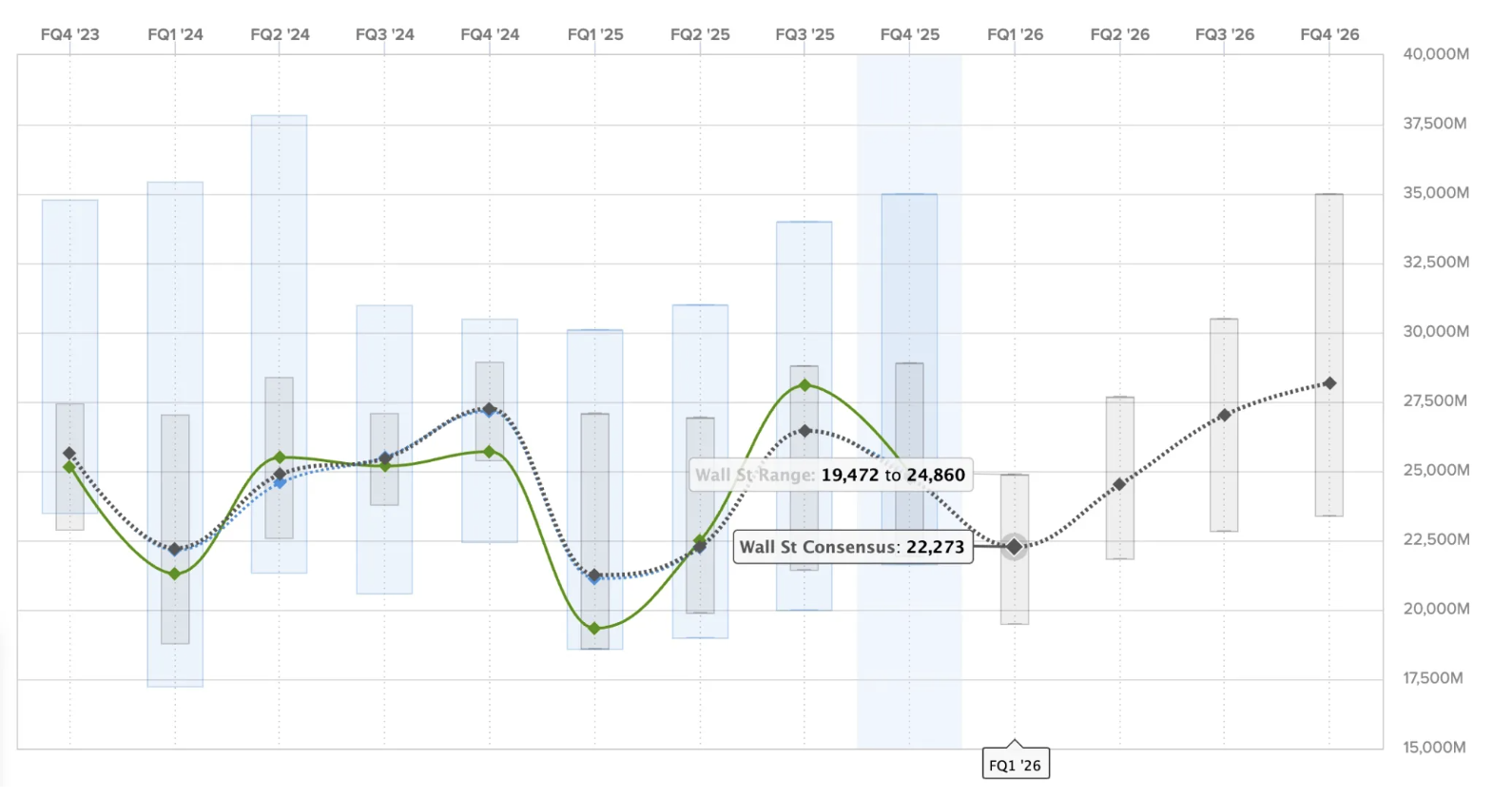

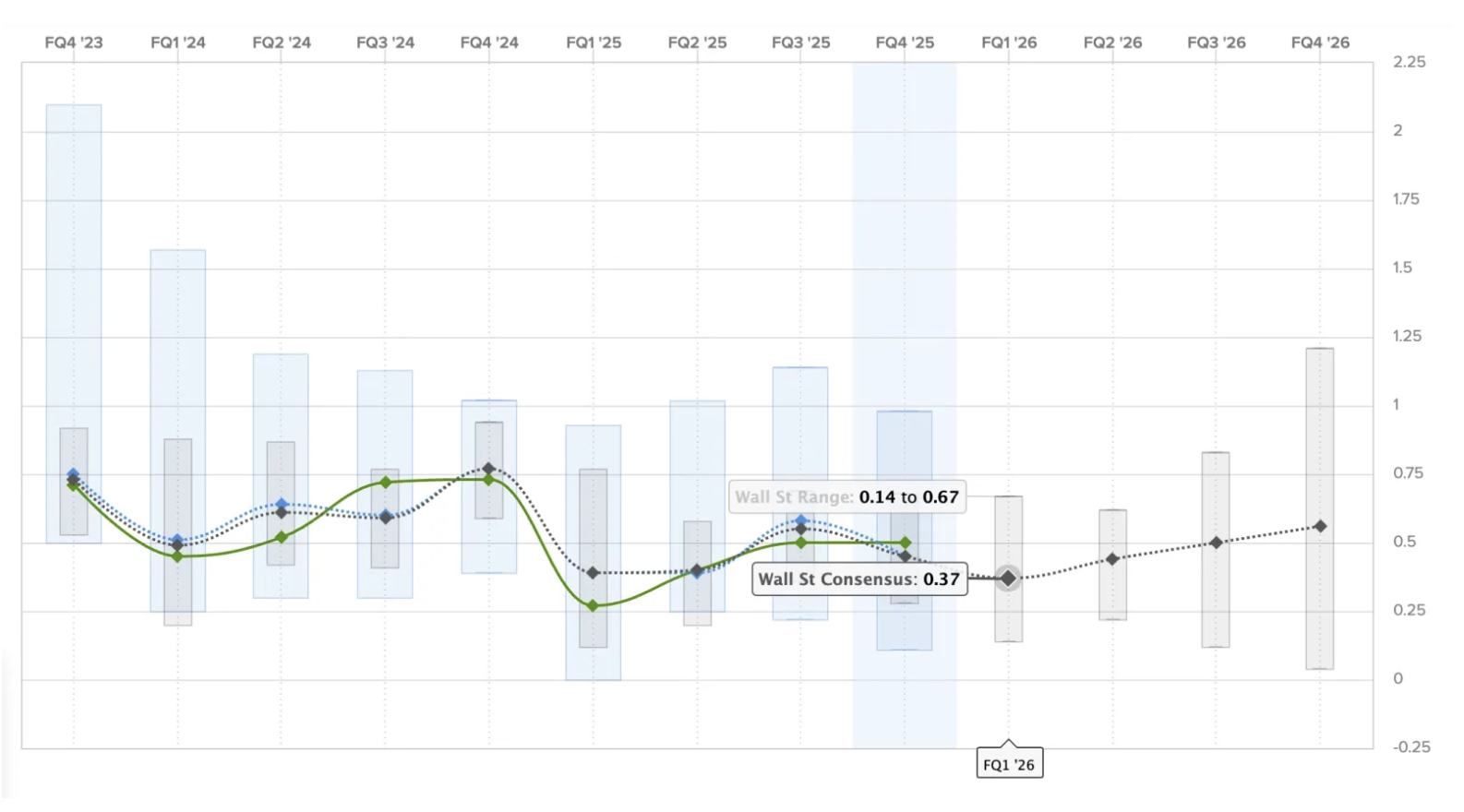

The company delivered 358,023 vehicles in Q1, about 7,600 fewer than the Street estimate of 365,645. Tesla produced roughly 50,000 more vehicles than it delivered in the quarter, creating an inventory build. Analysts expect Q1 earnings per share of about $0.36 to $0.37, while a Refinitiv smart estimate is near $0.30.

Revenue projections range from roughly $21.9 billion to $22.7 billion, up about 13% year over year but below fourth-quarter 2025 levels.

Automotive gross margin will be closely watched. Analysts have identified a 17% to 18% range as a key threshold; further declines toward 15% would reflect ongoing pressure from price cuts and competition from Chinese automakers such as BYD. Tesla plans more than $20 billion in capital spending in 2026, up from about $8.5 billion in 2025, with much of the increase aimed at AI compute and robotics programs.

Management has outlined three pillars tied to autonomy:

- Full Self-Driving software and a global rollout,

- Cybercab robotaxi network,

- Optimus plus the Dojo training system.

Regulatory approvals in Europe for supervised FSD deployments and the rollout of a Self-Driving App will be watched for take-rates and recurring software revenue. Cybercab prototypes have moved from Giga Texas to testing sites, and Tesla has identified Dallas and Houston as potential launch markets; investors will seek timing and revenue milestones. Shareholders will also monitor Optimus and Dojo for signs that heavy spending is producing measurable performance improvements rather than weighing on cash flow.

Tesla's energy-storage deployments reportedly declined sequentially in Q1; any rebound in that business would affect the company's revenue mix. Market analysts say a Q1 beat on EPS combined with a clear road map for robotaxi revenue could lift the stock toward late-2025 highs near $490 to $500. Conversely, continued margin erosion alongside aggressive CapEx could put pressure on the share price toward recent support around $355 to $360 or lower near $336.

Market analyst Zain Vawda wrote that Tesla’s Q1 results may be judged more on the company’s strategy than on the number of cars delivered. The April 22 earnings call will include management commentary and investor questions on how Tesla intends to convert its AI and robotics investment into recurring revenue.

The content on The Coinomist is for informational purposes only and should not be interpreted as financial advice. While we strive to provide accurate and up-to-date information, we do not guarantee the accuracy, completeness, or reliability of any content. Neither we accept liability for any errors or omissions in the information provided or for any financial losses incurred as a result of relying on this information. Actions based on this content are at your own risk. Always do your own research and consult a professional. See our Terms, Privacy Policy, and Disclaimers for more details.

Articles by this author